Alpha, Secondaries and Investors - Oh My!

There’s a strange optimism I keep hearing from managers about private secondaries, as if selling into the secondary market is some overlooked alpha strategy, and it just isn’t.

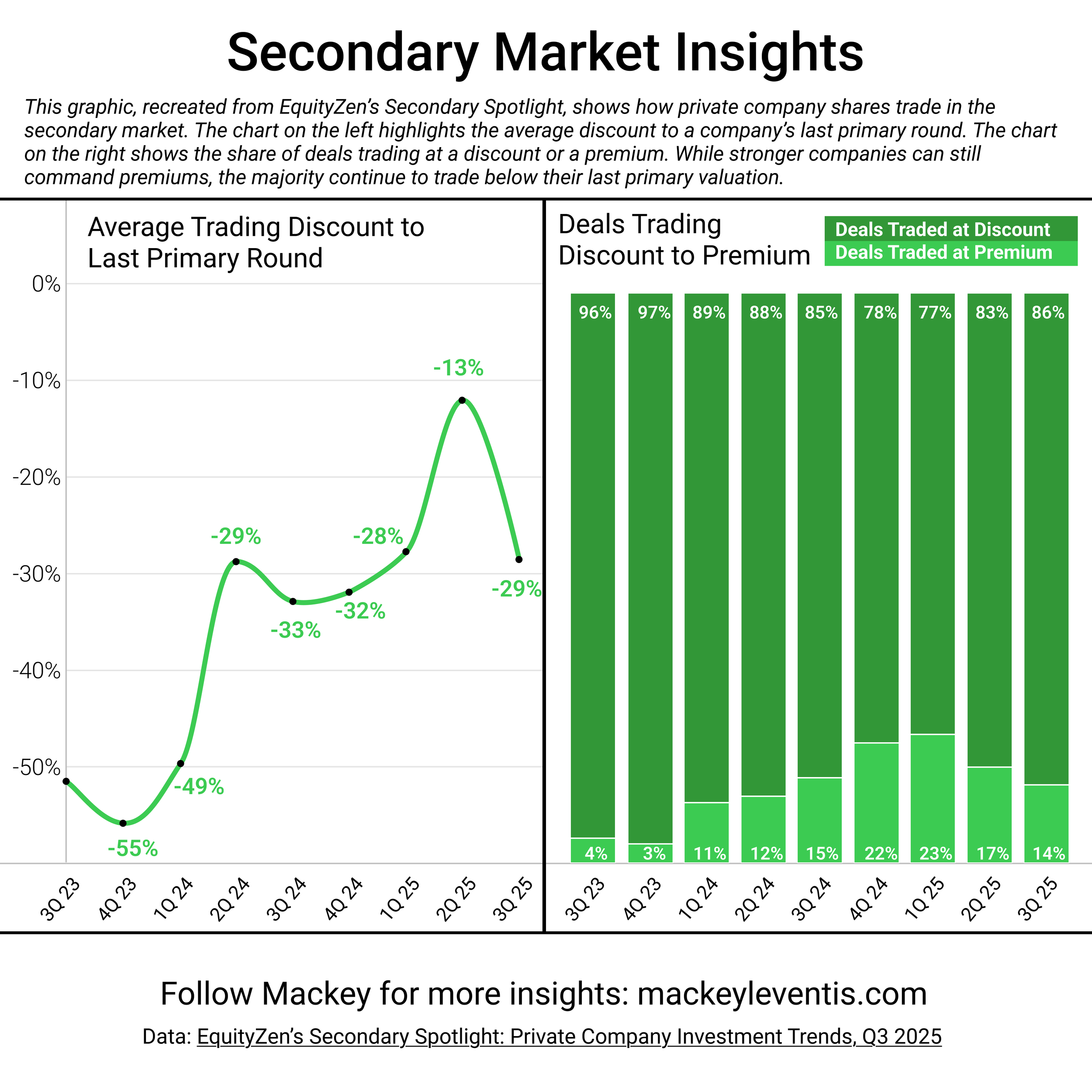

Premiums to Primary rounds rarely happen. Discounts are the norm. Buyers are looking for mispricing, and sellers are often in a pinch. Secondary buyers want the winners, not the leftovers. They want the assets with the most potential, the ones you expect to still return your fund...

I respect managers who get "creative" with liquidity, but it is worth remembering that short-term liquidity often comes at the expense of long-term returns.

Just check out the chart below from EquityZen's Q3 Secondary Spotlight.

A Proposal to Actually Generate Alpha in Venture

One of the last real sources of alpha in private markets is simple information asymmetry. This is not insider information. It is the advantage that comes from understanding how venture actually works at a deeper level than most managers.

Even after the number of active firms has dropped since 2021, many VCs still do not understand the fundamentals of their own asset class. They struggle with preferred stock mechanics, exit waterfalls, and even basic post money math. That lack of knowledge creates opportunity for those who truly understand the system.

Strong managers are not just good pickers. They understand securities, fund structures, and how value moves through a cap table. They know their real customer is the LP. They use structural knowledge to shape outcomes instead of waiting for the market to decide their returns.

Consider a basic concept the industry often forgets: common is not equal to preferred. Preferred carries rights like liquidation preference. Common is the residual. Yet many investors regularly pay preferred prices for common in secondaries simply to increase ownership optics. Large funds can afford this mistake. Emerging managers cannot.

If you understand how post money actually reflects the preference stack, how downside scenarios distribute value, how secondaries clear, and how discounts to NAV should be priced, you already have a meaningful advantage. You avoid overpaying for the wrong security. You avoid chasing short term liquidity at permanent discounts. You structure entries and follow ons in ways that protect downside and preserve upside.

Most people in venture talk about being founder friendly or building a platform. Very few use the mechanics of securities, capital stacks, and secondary pricing to generate quiet and repeatable alpha.

This is the opportunity. Information asymmetry is alpha.